[vc_row][vc_column][vc_column_text]

Life insurance is one tool farmers use to help equalize their estate. Below is a comparison of the different costs of buying your life insurance today rather than waiting until you’re older.

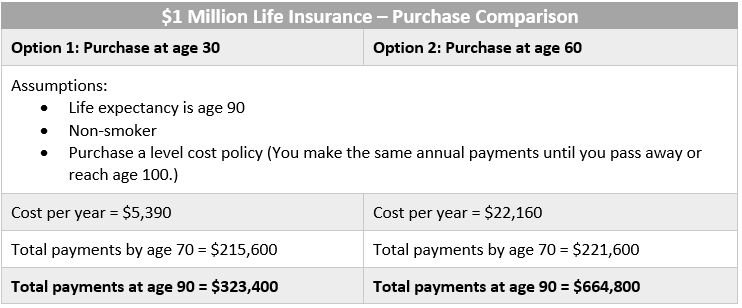

The scenario

You have two children. One would like to farm; the other one isn’t interested. You want to make things fair, but it doesn’t necessarily have to be equal. You’ve spoken with your team of advisors and you’ve decided to leave 100% of the farm to your child who’s interested in farming while leaving your non-farming child with $2 million in other assets. You have $1 million worth of non-farm assets, so you decide to buy a permanent $1 million life insurance policy to get you to that $2 million mark.

That’s quite a difference in cost! After age 70, you would save over $15,000 per year in payments by having started earlier. Hence, the large difference in total insurance costs by age 90 when comparing starting at age 30 to 60.

What if you wait until age 80 to buy insurance? You’d only have to pay for 10 years assuming you only live until 90, right? Sure, you can wait but it’s going to cost you $76,964 per year for a total cost of $769,640 at age 90. Never mind the fact that your cash flow would need to support a $76,964 premium each year. If you happen to live until 95, you will have paid $1,154,460 for your $1,000,000 life insurance policy.

The takeaway

The earlier you buy your insurance policy, the least expensive it’s going to be in the long run. You may say, “I have no idea how much insurance I’ll need when I’m 90.” That’s fine, nobody knows for sure when they’re 30, but it wouldn’t hurt to buy some today. For example, if you’re 30 why not buy $250,000 for $1,432 per year. Is $250,000 going to be enough? Probably not, but at least you’ll have some coverage locked in at a low annual price. Over the years as your farm evolves, your children grow up, and it becomes apparent you may need more insurance, you can always apply for more (assuming you’re still in good health).

Starting small today is a great way to relieve pressure on the farm in the future.

[/vc_column_text][/vc_column][/vc_row]