[vc_row][vc_column][vc_column_text]

If you’re planning to leave your employer due to your retirement or a change in career paths, then you may be faced with the decision to either take your pension as a lump sum or as a monthly income.

What is a defined benefit plan?

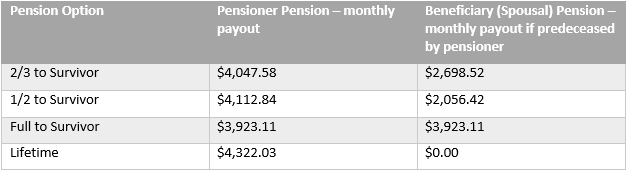

A defined benefit plan promises to pay a pre-determined amount upon your retirement until you pass away. If you’re married, you will be given additional options to support your spouse in the event you predecease them. See an example of such options below.

Alternatively, you can elect to bypass these options and choose to receive a lump sum payout instead. By choosing to pull (commute) your pension money out of your employer’s plan, you will have the opportunity to invest the funds yourself or with the help of a financial advisor. There are pros and cons to each option.

Today, we’ll examine five reasons you should commute your pension.

1. Pension Sustainability

How is your pension plan holding up today? Your annual pension statement should contain information on your pension’s solvency test. If the result is anything less than 100%, the pension may not be able to meet all of its obligations to pensioners. If the solvency test shows a result of 70%, how will the pension make up the 30% gap so that all pensioners receive what they were promised?

It’s important to review the sustainability of your pension, but it’s equally as important to consider where your company will be in the next 20 to 30 years. We’ve all heard the terrible stories of pensioners having their pensions cut in companies such as General Motors, Nortel, and Sears. If there’s any risk of your company becoming obsolete while you are retired, it may make sense to pull your pension rather than potentially having your monthly benefit reduced.

Even if your company is still around in 20 years, will they be the same company as today? If the work were to become automated, who would be contributing to the pension to ensure it remains stable? Do robots make pension contributions?

2. Flexibility

The scenario:

Let’s say you’re 63 and ready to retire. You have the option of receiving $5,000 per month from your pension until you pass away. This sounds ok, but you’d like to have the option of receiving a higher payout today while you’re still healthy and a lower income in your 80s when you will likely need less to sustain your lifestyle.

If you take the monthly payments:

Unfortunately, the monthly pension does not allow for this sort of income manipulation. Assuming your pension is indexed, your income will be at it’s highest in the later years of your retirement. This could potentially cause a clawback of income-tested benefits such as Old Age Security.

If you take the lump sum payout:

Pulling your pension would grant you a lot more flexibility when it comes to your income. There are rules which dictate how much you are allowed to withdraw from your locked-in accounts, but there are ways to access these funds. See What happens when you withdraw your pension for more details.

For example, you could elect to withdraw $7,000 per month during the first 15 years of your retirement to support increased expenses for travel with the understanding that you would only withdraw $3,000 per month after that. However, a proper review with a Certified Financial Planner should be completed before implementing such a strategy.

3. Your Age

Deciding between the monthly pension and the lump sum doesn’t always occur upon retirement. In some cases, such as a career change, you may be forced to make a decision a lot sooner than you might expect.

The scenario:

Let’s say you’re 40 years old and changing your career path. You can elect to leave your pension as is and begin to receive a monthly payment of $3,000 per month in (today’s dollars) at age 55. Alternatively, you could take your pension as a lump sum payout in the amount of $400,000 today.

If you take the monthly payments:

If you choose the monthly payment option, the $3,000 payment will increase until you begin taking the pension (let’s assume this to be at age 55). Generally, in Manitoba, the indexation of the pension benefit is based on the Consumer Price Index (CPI). If the index goes up 2.5% in one year, you can expect to pay roughly 2.5% more for the same goods and services that you purchased last year.

In most plans, the benefit increase is limited to a maximum of 2/3 of the yearly CPI. Therefore, if the CPI is 2.5%, the maximum annual increase in the benefit would be 1.65%. If the maximum increase is received over the next 15 years, the value of the $3,000 monthly payment offered today will be reduced.

If you take the lump sum payout:

On the other hand, if the lump sum payout option is taken today, those proceeds can be invested with the opportunity of outpacing inflation and increasing your purchasing power at age 55.

4. Shortened Life Expectancy

One of the points to consider when deciding between the monthly pension and the lump sum is your life expectancy. If you don’t have a history of longevity in your family or are currently dealing with health issues, it may be beneficial to take your pension as a lump sum payout.

The scenario:

Let’s consider the following; you are retiring at the age of 60. You’ve worked for the same employer for the last 35 years and have the option of taking monthly pension payments of $4,000 or pulling your pension and receiving a lump sum payout of $900,000. During your 35 years of employment, you contributed $150,000 to your pension plan.

If you take the monthly payments:

Let’s assume you elected to take the monthly pension and passed away after three years. Your total withdrawals from the pension (without taking into consideration any indexing) would be $144,000. Since you had contributed $150,000 to the pension plan while you were working, your estate would receive an additional payment of $6,000 to match your pension contributions. There would be no further payments from the pension plan, even though you only had three years of withdrawals.

If you take the lump sum payout:

Comparatively, had the lump sum option been chosen, there would be significantly more funds left over for your estate assuming the same withdrawals.

5. Control

If you leave your funds in the pension plan, you can’t stop the pension board from investing in Company X, which is spilling oil into the ocean. And forget about asking for a higher payout for a year because you have a once-in-a-lifetime trip planned.

By taking the lump sum payout, you remain in control of your money. You decide how or in what company your funds are invested, how you receive your retirement paycheque, and how your funds will be dispersed upon your death.

You’ve worked hard for your pension. Haven’t you earned the right to decide how it’s managed?

If you have any questions about your personal situation, please don’t hesitate to get in touch.[/vc_column_text][/vc_column][/vc_row]