You’ve done the hard part. Now it's about making your retirement decisions work together

Most Canadians reach retirement having saved well.

What catches many people off guard is how one retirement decision often affects several others.

A CPP decision can affect your withdrawal strategy. A withdrawal strategy can affect your taxes. Those taxes can affect what you’ve spent decades building.

That’s why your retirement decisions need to work together.

Retirement decisions around CPP, withdrawals, and income structure can affect your taxes and flexibility for decades.

Early in retirement, you often have the most control over how income is structured and where it comes from.

Over time, some of that flexibility starts to narrow.

The earlier these decisions are coordinated intentionally, the more options tend to stay available later.

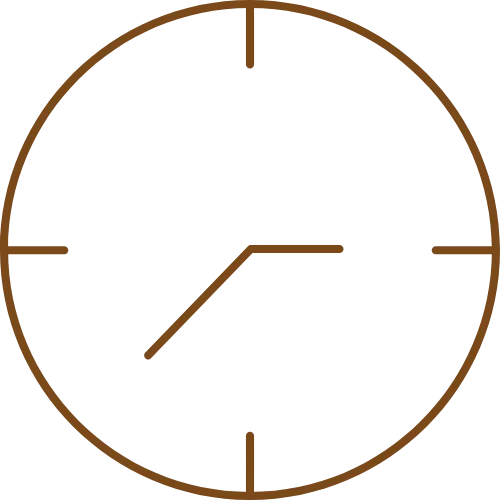

Early 60’s

CPP now or later?

What does each option cost over time?

Mid 60’s

Use RRSP Money Now?

Could it lower taxes later?

Late 60’s

Income stacking up?

Am I paying too much tax?

Early 70’s

RRIF withdrawals starting?

Do I still control income?

THE TEAM

Advice That Works Together

You’ll work with CFP professionals, portfolio managers, and an in-house CPA who coordinate retirement income, investments, and tax decisions together.

As retirement evolves, your strategy evolves with it. Ongoing reviews help ensure that income, investments, and tax decisions continue to support the bigger picture over time.

COORDINATION REVIEW

It’s time to see how your retirement decisions work together.

We’ll learn more about your situation, discuss what’s important to you, answer your questions, and explore whether the Atlas System is the right fit for your retirement.

30-minute introductory call

No preparation needed

No obligation to move forward

Trans Canada Wealth Management provides retirement income planning and investment management for Canadians approaching retirement. Our focus is on coordinating your income, investments, and tax decisions in retirement so unnecessary taxes are avoided. This includes: CPP & OAS timing; RRSP withdrawals from investment accounts such as RRSPs, RRIFs, TFSAs, LIRAs, and LIFs; proper investment allocation; tax planning; and estate planning. Our goal is to create a steady income for you throughout retirement that is stress tested against inflation, market volatility, and is flexible enough to change along with you during your retirement.

What is retirement income planning?

Retirement income planning is the process of turning your savings into reliable income throughout retirement. It involves deciding when to take CPP and OAS, how to withdraw from accounts like RRSPs and TFSAs, and how to manage taxes so your income lasts.

When should I start CPP?

The right time to start CPP depends on your income needs, tax situation, and life expectancy. Starting earlier provides income sooner but at a reduced amount, while delaying CPP can increase your payments.

There isn’t a one-size-fits-all answer. The only way to make the right decision is to look at your full financial picture, including your other income sources, investments, taxes, and personal goals, so the timing works for you.

How are RRSP withdrawals taxed in retirement?

RRSP withdrawals are fully taxable as income in retirement. The amount you withdraw can affect your tax bracket and may impact benefits like OAS. Planning when and how much to withdraw is important to reduce taxes over time.

What is a tax-efficient retirement strategy?

A tax-efficient retirement strategy focuses on reducing the total tax you pay over time. This includes coordinating withdrawals from different accounts, managing your income levels, and timing benefits like CPP and OAS so your decisions work together.

What matters most in retirement is how much you keep after tax, since that’s the income you actually have available to spend. The goal is to structure your plan so that more of your money stays in your pocket over time.

Why is it important to coordinate retirement decisions?

Retirement decisions are connected. Choices around CPP, RRSP withdrawals, investments, and taxes all affect each other. When these decisions are made separately, it can lead to unnecessary tax and missed opportunities. Coordinating them helps improve outcomes.