[vc_row][vc_column][vc_column_text]Much like the summer months, December seems to come and go in the blink of an eye. We’re all so busy with work events and family gatherings that

year end tax planning often gets neglected. With COVID forcing most of us to stay home this year, we can all use this opportunity to make sure our tax

plans for 2020 are in order.

Over the next few weeks, I’ll share four strategies (often overlooked by advisors) that you should consider implementing before the end of the year.

The majority of people have contributed to RRSPs at some point or another. What’s the best way to draw them down? Without further ado, the first tax

planning strategy.

Tax Planning Strategy #1: RRSP/RRIF Withdrawal

One of the major drawbacks of owning an RRSP or RRIF is the potential tax bomb it creates.

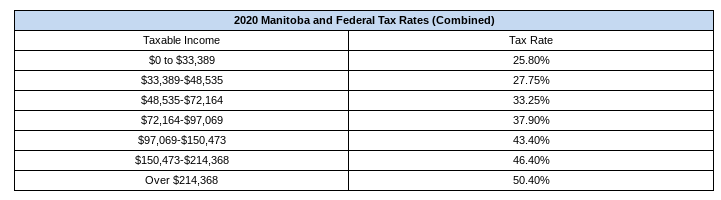

To understand the tax bomb, let’s first look at the combined Manitoba and Federal Tax Rates.

Ron makes $100,000 per year, which puts him in the 43.4% tax bracket. A common misconception is that Ron will need to pay 43.4% tax on all his

income. That is not the case; Ron will only pay tax at 43.4% on his income from $97,069 to $100,000. On the rest of his income, he will pay at the

corresponding rates in each bracket. When we factor in these brackets, Ron’s average tax rate is only 28.34%

The Tax Bomb

Jim and Val are retired, and they each make $60,000 per year. This puts them in the 33.25% tax bracket.

They each have $500,000 in their RRSPs, and when either Jim or Val pass away, they can roll over their RRSP to their spouse tax-free.

Jim passes away, and his $500K in RRSPs transfers to Val’s RRSP tax-free. At this point, Val’s RRSP is worth $1,000,000.

The downside of an RRSP or RRIF is that upon the death of the second spouse, everything in the RRSP becomes taxable.

If Val were to pass away with $1,000,000 in her RRSP, it would all be taxable in one year, and her estate would end up paying over 50% tax on a large portion of it. Wouldn’t it be great if you didn’t have to pay tax at over 50%?

Thankfully you can!

If Jim and Val each withdrew an extra $12,000 from their RRSPs, their incomes would increase from $60,000 to $72,000. A withdrawal of this size would

keep them both in the 33.25% tax bracket today.

The advantage of this extra withdrawal (even if they don’t need the funds) is that it allows them to withdraw funds from their RRSP at 33.25% rather than potentially paying over 50% in the future.

I’d rather keep those savings in my family’s pocket rather than it going to the CRA.

Stay tuned for Part 2, where I’ll be going over why in some cases, it’s advantageous not to purchase investments until the new year.

[/vc_column_text][/vc_column][/vc_row]