Sometimes withdrawing more is the best strategy.

Introducing Daniel

Daniel worked hard all his life, so by the time he retired he had accumulated a healthy amount of savings in his RRSP. It’s not because Daniel had an overabundant cashflow. There were years where he had to choose between replacing his TV or contributing to his RRSP. He always chose the RRSP and looking back he’s sure happy he didn’t buy that one ton 50-inch bubble tv. It would still be in his basement as there was no way he could carry that thing back up the stairs.

Now that Daniel is retired, he’s mentally having a hard time withdrawing from his RRSPs. He knows that every dollar withdrawn is considered taxable income, so he only withdraws the bare minimum for his desired lifestyle. Usually, this would be good tax planning on Daniel’s part to avoid paying extra tax. But today we’re going to examine why in some cases, it makes sense to withdraw more from your RRSP.

The Scenario

Daniel and his wife are both 67 years old and they each have their individual RRSPs valued at $500,000. They’ve both had health issues in the past and don’t come from families with longevity. Daniel receives $55,000 a year from his pension, his OAS (Old Age Security), and CPP (Canada Pension Plan). He also withdraws $5,000 from his RRSP for an annual trip to Mexico. This brings his yearly income to $60,000, the minimum necessary to maintain his lifestyle going forward.

The Issue

Daniel’s withdrawals of $5,000 per year is 1% of his $500k RRSP. If the investments within his RRSP grow at a higher rate, his RRSP will continue to grow in value. This is great news on one hand, but from a tax perspective, it could result in a massive tax bill in the future.

The issue occurs upon death. If Daniel stays this course (Scenario 1 below) and his wife was to pass away, her RRSP would be rolled over to him tax-free. At that point, Daniel would have an RRSP valued at $1M. Once Daniel passes away, the entire value of the RRSP would be considered taxable income upon his death. Daniel’s estate would have to report an income of $1M and would lose a significant portion to taxes.

The Strategy

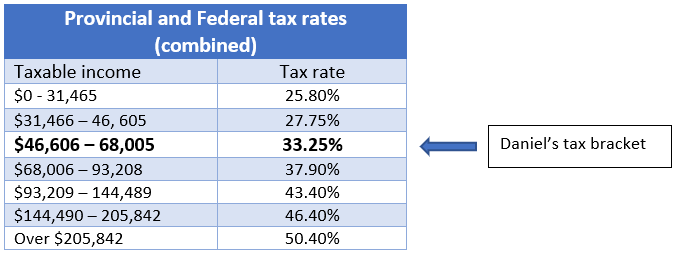

Using the Manitoba/Federal tax rates (see table below), Daniel’s income of $55,000 puts him in the 33% tax bracket. When Daniel withdraws from his RRSP, he ends up owing just over $1,500 in taxes. As mentioned, the $5,000 withdrawal brings Daniel’s income up to $60k because a withdrawal is considered taxable income.

In this instance, I would suggest that Daniel withdraws an additional $8,005 ($68,005 – 60,000) from his RRSP (Scenario 2 below). This would bring his income to the top of the tax bracket but would allow him to pay the same amount of tax per dollar as he is currently paying. The more he’s able to withdraw from his RRSP today, the less tax Daniel’s estate will have to pay upon his death.

The Payoff

Daniel can use the additional funds from his RRSP withdrawals to maximize his TFSA. The benefit of maximizing your TFSA is that there will be no tax owing upon death.

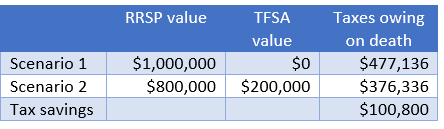

Here’s a quick look at the potential tax savings Daniel could benefit from if he uses this strategy for a few years.

Wrapping It Up

If you’re currently withdrawing from your RRSP or RRIF, this tax-saving strategy could potentially save you thousands of dollars. That means more can be left for your family or favorite charity. As always, an extra dollar in your family’s pocket is better than in someone else’s.