Portfolio Manager, Certified Financial Planner®

Congratulations on reaching this milestone! Whether you’re considering retirement or already retired, planning how to draw from your savings is crucial. Here are some valuable tips for making tax-efficient retirement withdrawals. These insights will help you maximize your financial resources and enjoy your retirement to the fullest.

We will look at how to make tax-efficient retirement withdrawals, providing you with the knowledge and strategies you need to navigate your retirement. Let’s dig in!

Retirement isn't just about leaving the workforce; it's about optimizing your income streams and minimizing your tax burden to make the most of your hard-earned savings.

Before starting to plan, think about what you want out of retirement. Retirement means different things to different people. Some may dream of traveling the world, while other may envision hosting the family at the lakeside cabin. Take some time to ask yourself:

Once you know what you want out of retirement, how much is it going to cost you?,

More importantly, when is it going to cost you?

Most retirees end up having staggered expenses throughout retirement.

More money is spent upfront, while health is usually at its best and less on the back end of retirement.

Figure out how much your retirement will cost, download our budget calculator via the link below

Now that you have an idea of what retirement looks like for you, its time to assess your financial reality. This involves taking stock of your current assets including:

Savings and Investments: Calculate the balances in your retirement accounts, savings accounts, and investment portfolios.

Pensions and Government benefits: If applicable, understand the benefits you’ll receive from employer pensions and government programs such as CPP or OAS.

Debts and Liabilities: Don’t forget to account for any outstanding debts or financial commitments.

Real Estate: Assess the value of your primary residence and any other properties you own.

Other Assets: Include any other assets, such as valuable collectibles, or businesses.

If you haven’t started your CPP or OAS, you can find out what you are on track to receive by visiting My Service Canada (MSCA). You’ll need to register first if you haven’t already done so Alternatively, you can find out what you are on track to receive by calling 1-800-277-9914. Make sure to have your SIN number handy when you call them.

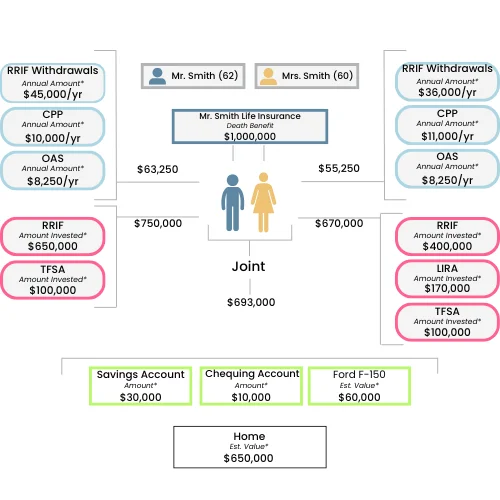

To stay organized, I would suggest creating a visual (Asset Map) such as the example below. Additionally, this can be used to make sure spouses are on the same page with their financial picture. A copy can also be kept with your will, so your executor knows where your financial assets are located.

To put it bluntly, you now know what you want and what you have. It’s time to craft a retirement plan that bridges the gap between the two. Here’s what you’ll need:

With this information, you can figure out whether you’re on track to achieving your retirement goals.

Now that you have an outline of a plan built, how can we optimize it from a tax perspective?

Let’s first shed light on RRSPs (Registered Retirement Savings Plans) and RRIFs (Registered Retirement Income Funds). If you’re planning for retirement, these acronyms are likely on your radar, but the intricacies of how they work might still be a bit hazy.

Let’s break down the key differences between them and help you understand the nitty-gritty details of making withdrawals. By the end of this video, you’ll have a solid grasp of how to access your retirement savings smartly and efficiently. So, let’s dive in and demystify the world of RRSPs and RRIFs!

Now that we understand the difference between RRSPs and RRIFs let’s review some of the landmines that you should be aware of.

RRSPs are a great tool to save for retirement, but if not used properly in retirement, you could end up with a significant tax bill. In some cases, you can end up paying over 50% tax on your withdrawals. In this video, we review how to effectively plan your RRSP and RRIF withdrawals.

Wouldn’t it be nice if you could make withdrawals from your RRSP or RRIF tax-free? In some scenarios, you can!

In this video, we explore a strategy that you can take advantage of if you have a low-income year in retirement.

We often utilize this strategy when one spouse is working while the other is retired.

An unfortunate reality is that, in some cases, your life expectancy may be shortened due to a variety of factors.

As we’ve alluded to in previous videos, this could lead to a significant tax bill for your estate. In this video, we review a strategy to minimize that tax bill when facing a shortened life expectancy.

How much should you be withdrawing from your RRSPs or RRIF on a yearly basis to reduce your tax bill throughout retirement?

It all depends on the tax bracket you’re in today and which tax bracket you can expect to be in the future.

To ensure no surprises, it’s best to wait until the end of the year to make these withdrawals as you’ll have a better idea of your taxable income

If you’re in a position where your estate is facing a 50% tax bill, it can be easy to become overly aggressive with your RRSP and RRIF withdrawals to eliminate this tax bill.

However, being overly aggressive with your withdrawals can have a significantly negative impact on your bottom line.

It’s best to build out a plan to withdraw the optimal amount on a yearly basis.

When it comes to your overall portfolio, you’ll likely have other accounts to draw on as well, whether that’s a non-registered account, a TFSA, or a corporate account.

How do you determine how much and which accounts to pull from in retirement?

In this video, we review how to decide which account to draw on to create the income that you need in retirement while keeping your tax bill as low as possible.

Now that we have a good base understanding of what we need to factor into a retirement withdrawal strategy, let’s go through a real-life example to see how these strategies can impact your bottom line.

As we take it a step further, we can further optimize a withdrawal strategy once we know the order of our withdrawals.

In this video, we go over some key considerations when it comes to how each of your accounts are invested. If there are certain accounts that won’t be used for many years, they shouldn’t be invested in the same manner as the accounts you plan on using in the coming years.

Lastly, let’s review how you can use a bucketing approach in retirement.

For many of our clients, this is an approach that has reduced their stress levels when thinking about their retirement portfolio.

By implementing this approach, you can focus on the passions and experiences you want to enjoy in retirement.

Needless to say, having a proper withdrawal strategy in place can save you thousands if not hundreds of thousands in taxes throughout your retirement.

Together, we’ll keep more money in your pocket by creating a personalized withdrawal strategy that minimizes taxes, optimizes your income, and helps you enjoy the retirement you deserve. Let’s make your retirement work for you

Book a free, no-obligation meeting today.

Trans Canada Wealth Management is a Winnipeg-based financial advisory team with Harbourfront Wealth Management. The team works with pre-retirees and retirees seeking guidance on retirement, investments, and taxes.

The views expressed are those of the advisor(s) featured and not necessarily those of Harbourfront Wealth Management Inc., a member of the Canadian Investor Protection Fund.

AssetMap is a free financial planning service that allows users to develop a snapshot financial roadmap through a series of questions. Our advisors can use this financial snapshot as one of many tools to build your financial plan, however it is not to be considered a substitute for consultation with professional accounting, tax, legal or other professional advisor. Transcanada Wealth Management and Harbourfront Wealth Management inc. are not partnered with AssetMap, though we pay a subscrpition fee for use of their maping software. Information is provided to Asset Map at the client’s discretion and may be used by Asset Map subject to their own terms of service and company policies.