[vc_row][vc_column][vc_video link=”https://youtu.be/6lPhNQyQ1Zk” css=”.vc_custom_1615869473595{padding-top: 20px !important;padding-bottom: 20px !important;}”][vc_column_text css=”.vc_custom_1611901511867{padding-bottom: 20px !important;}”]I’ve had the pleasure of working with several clients who work or have retired from Manitoba Hydro. While each person’s financial situation is different, some commonalities exist amongst those sharing and employer. This guide identifies those shared characteristics and provides advice regarding their financial planning implications.

What makes your financial situation unique?

As an employee of Manitoba Hydro, your position has several interesting financial planning implications: a 9-day work cycle, a great pension plan, a northern allowance, relatively high pay compared to the average worker, and exceptionally good health benefits.

Given the demanding nature of your job, as well as the advantage of a great pension plan, I often see Manitoba Hydro employees put the management of their finances on the back burner. I would strongly urge you not to. You have a real opportunity to take advantage of your financial position and set yourself up for the retirement you’ve always dreamed of.

Many of you have worked at Manitoba Hydro for many years. This puts you in a position to retire as early as age 55 without having your benefits reduced (assuming you meet the “Rule of 80”). This creates a unique financial planning opportunity as you may have a retirement lasting over 40 years.

By optimizing your portfolio, minimizing your taxes, and maximizing your income potential today, you can take advantage of the long term impacts of compounding.

Your analytical capacity also sets you apart. Like many of my clients, I’m sure you know your way around an Excel spreadsheet and can analyze certain decisions that most people would only guess at.

On the other side of the coin, this can cause overconfidence. As is likely the same in your field, knowing a bit about something is sometimes worse than not knowing anything at all. With the proper guidance and your brainpower, you’re certainly better positioned than most to manage your finances.

Developing a well thought out plan is vital at this stage of your career. I hope this guide helps.

The Six Questions You Need to Answer

1. When can I retire?

Without a doubt, this is the most frequent question I receive from Manitoba Hydro employees. Unfortunately, there isn’t a quick and easy way to answer it. Many factors come into play, and it truly depends on the lifestyle you want to have in retirement.

If you plan to have an expensive lifestyle, which includes frequent travel, you’ll likely have to work longer than most. If you’re the type of person who has a modest lifestyle, you will be able to retire a lot sooner.

Use the following three steps to determine if you’re on track.

Step 1: Find out what your monthly expenses will be in retirement. Having a hard time thinking of all your possible expenditures? Download our budget calculator Excel sheet here to go over a list of common expenses.

Step 2: Determine what income sources you (and your spouse, if applicable) will have in retirement. This generally includes:

- CSSB Manitoba Hydro Pension

- CPP

- OAS

- RRSPs and RRIFs

- Tax Free Savings Account

- Home Equity

Step 3: Calculate at what age these sources of income will be sufficient to sustain your retirement expenses.

Proceed with caution. If you plan to model these projections yourself, be aware that it’s extremely difficult to project 40+ years in the future. Before making any decisions, I would recommend consulting with a Certified Financial Planner as they have the right financial planning software to model your retirement plan. You don’t want to make an error that forces you to have to go back to work.

Their software can account for variable investment returns, increases/decreases with the rate of inflation, and adjustable tax rates based on your income. They will also be able to adjust your plan to account for numerous scenarios such as:

- Downsizing your home

- Buying a retirement property

- Unexpected death

- Variable medical expenses

As previously mentioned, the sooner you put a plan into place, the more quickly you can take advantage of the improved efficiencies, which leads to greater long-term compounding.

2. Which pension option should you choose?

If you’re part of the Manitoba Hydro CSSB pension, you’ll have the option to take your pension as a lump sum payment (commuted value) or as a lifetime monthly benefit. If you are part of the Winnipeg Civic Employees Benefits Program, you will only have the monthly benefit option available to you.

Part of the CSSB pension, which option should you choose?

There isn’t a universally accepted answer when deciding between these two options, as it mostly depends on your personal circumstances. Just because a retired co-worker chose one option, doesn’t mean the same choice is right for you.

Several factors could affect your choice, so an excellent place to start would be to build a financial plan. This will allow you to compare the short and long term financial implications between both options. Having said that, even if one option seems better financially than the other, that doesn’t always mean that it’s the correct choice. Other factors come into play that must be analyzed before making your final decision. For a complete analysis, click here.

The value of your monthly benefit is determined based on different variables, such as your years of service and your average pensionable salary. It’s fairly easy to project the value of your pension upon retirement as you can plug in your own variables.

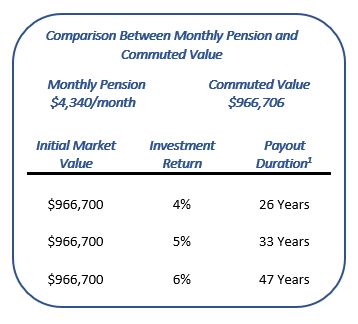

When it comes to commuting your pension, the value of the benefit changes every day as it is tied to interest rates. Lower interest rates generally mean higher commuted values. Why?

Let’s say you needed $60,000 per year. If interest rates were at 10 percent, you would need to invest $600,000 to generate the $60,000 you required. If interest rates were only at 1 percent, you would need to invest $6,000,000 to generate $60,000 per year.

When interest rates are low, the pension plan must pay you a larger amount to match what the monthly benefit would pay you. With interest rates extremely low at the moment, now would be a good time to look at this option.

Once you have the cash, if you invest it in a conservative portfolio, you have a great opportunity to increase the value of your pension.

1. Monthly Withdrawals to match monthly pension indexed by 1% per year

3. When is the best time of the year to retire?

By choosing the wrong retirement date, you could be leaving a lot of money on the table. Here are a few factors you should consider.

Vacation Days

At the time of your retirement, you will be paid out a lump sum amount for up to 50 days of unused, accrued, and banked vacation time. These vacation days count towards your pensionable earnings, which can increase your pension by as much as 4-5%. That’s a huge number when factored over the next 30 years.

The Manitoba Hydro fiscal year goes from April 1st to March 31st. If you haven’t accumulated your 50 days of vacation, consider waiting until April 1st to retire. This is the start of a new fiscal year, so you will be provided with another year of vacation time that you can use towards your 50-day allotment.

The vacation payout will be subject to tax and is generally paid out soon after you retire. This can be a substantial amount, depending on your hourly rate.

Sick Leave Vesting and Severance Plan Credits

Upon your retirement, you will also be eligible to receive a payout for your sick leave and severance plan credits. You can elect to receive a portion of the payout in the year you retire and each of the two years following your retirement.

If you expect to have a high income in the year you retire, it will make sense to defer these payments over the following two years when you’d likely be in a lower tax bracket. These payouts can add up as well, so you should elect to receive payment in a year where you will have a low income.

Factor in your salary for the year

If you were to retire on November 1st, you would have nearly a full year of income from working; After adding your vacation payout, you could be unnecessarily increasing your income in your retirement year. This would result in more taxes than necessary being paid

If you retired on January 1st or April 1st, your income from working would be substantially lower. The payouts from your vacation days, sick leave, and severance wouldn’t be subject to as much tax.

4. Should you work with an advisor?

Even though I’m an advisor, I will say that hiring one is not for everyone.

Some people genuinely enjoy this aspect of their life, and they treat it as a personal hobby. If you enjoy putting together projections and reviewing different tax strategies and investments; then, you should take the do-it-yourself approach.

If you feel you don’t have the knowledge, expertise, or more importantly the time, then you should hire someone to help you with this aspect of your life. You will likely be in a better financial situation without the stressful headache of taking this on yourself.

With that in mind, you have to make sure you hire the right advisor. After all, a bad one is probably worse than no advisor at all. If you needed heart surgery, would you call a heart surgeon or your family doctor? I think the answer to that question is fairly obvious. Many advisors are generalists and work with all types of people. Does the advisor know a little about a lot of things or a lot about one specific thing?

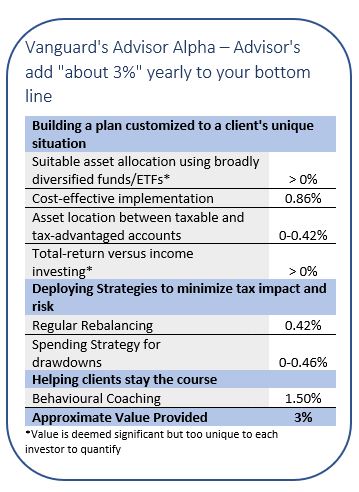

I would recommend you hire the advisor whose an expert in your field and who works exclusively with people in the same financial situation as you. They will be able to provide you with significantly more value, which will far outweigh their costs.

https://www.vanguardcanada.ca/documents/quantifying-your-value-to-clients-advisor.pdf

5. Should I accept an early retirement package

Manitoba Hydro has offered voluntary departure programs in the past. If they do so again, you’ll want to be prepared to make a decision. These offers are generally available for a limited amount of time, so you don’t want to be in a position where you have to scramble to put a retirement plan together at the last minute.

These programs will usually have financial incentives tied to them as they want you to accept the offer so they can reduce costs and staff. If you are approaching your expected retirement date, these incentives may put you in a position to achieve your financial goals much sooner.

Before deciding, there are many questions to be addressed. All of which are specific to individual preferences and circumstances. Here are eight such considerations to factor in before making your final decision.

- How does the package compare to what you would have received upon your planned retirement date?

- Will the package provide continued health benefits and insurance?

- What are the tax implications of the offer?

- Are you able to negotiate a better package?

- What happens if you don’t accept the early retirement offer?

- What will you do with your time if you retire?

- Are there other jobs available that could provide you with a similar income if you still want to work?

- What impact will this have on your financial future?

6. Should I be contributing to RRSPs

The RRSP has been getting a lot of negative attention over the last few years as people now realize that they have to pay tax on amounts withdrawn in retirement. Does that mean you should avoid the RRSP all together and focus your retirement savings in a TFSA instead?

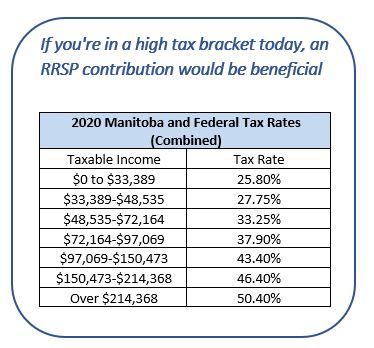

In some cases, that absolutely makes sense, but if you’re in a high tax bracket today, then RRSPs are still beneficial.

At its core, a contribution to an RRSP will reduce your taxable income by your corresponding marginal tax rate. For example, if you make $150,000 per year, you will fall under the 43.4% marginal tax bracket as per the combined 2020 Manitoba and Federal tax rates.

If you make a $20,000 contribution to an RRSP, your taxable income will drop to $130,000. This would result in a tax refund of $8,680 ($20,000 x 43.4%).

Let’s assume that when you retire, you have an income of $75,000 per year, including your pension, CPP, and OAS payments. When you withdraw that same $20,000 from your RRSP, it gets added to your income. This would increase your income from $75,000 to $95,000, and you would fall under the 37.90% tax bracket. The $20,000 withdrawal from your RRSP would cost you $7,580 ($20,000 x 37.90%) in taxes.

In this case, you would have tax savings of $8,680 when the $20,000 is deposited into your RRSP, and you would pay $7,580 when that same $20,000 is withdrawn from the RRSP. That’s a difference of $1,100 in your pocket!

What’s the next step?

You have the unique opportunity to take advantage of your financial position to set yourself up for the retirement you’ve always dreamed of.

If you would like to review your personal financial situation, I can be reached at (204) 256-5555 or by email at msabourin@harbourfrontwealth.com

[/vc_column_text][/vc_column][/vc_row]