Certified Financial Planner

Every farmer has a $1,000,000 capital gains exemption. Assuming your farmland is qualified farm property (you should always double-check with your accountant if you’re planning on selling) you can reduce your taxable gain by $1,000,000.

But what happens if your gain is much higher than your $1,000,000 exemption? Any gains above $1,000,000 will be taxable to you, so what can you do?

With enough planning, you’re able to get your children involved (assuming you trust them – more on that later) and use their capital gains exemption room to shelter the rest of your gain.

Here’s how it works. At least three years before you plan to sell, transfer your farmland to your children. Since the farmland is qualified farm property, it’s able to be transferred without triggering any taxes.

Fast forward three years. Since your child has been holding the land for the past three years, they’re able to use their capital gains exemption when the land is sold to a third party. It’s that easy but does require planning ahead of time.

If you’re wondering, “is it fair to use my children’s capital gains exemption for my benefit?” here are my thoughts.

First, your child won’t be able to use their capital gains exemption unless they build a business themselves and sell it in the future.

Second, who knows if this exemption will be around forever. All it takes is one government to take it away.

Lastly, if you’re concerned about it, give your children the tax savings you generate by using their capital gains exemption today. If I were your child, I’d much rather someone pay me to use my capital gains exemption today vs. waiting until I’m at a point in my life where I’m ready to use the exemption myself. I could do so much more with money today vs. receiving a tax break in my 60’s when I sell my business. Your alternative is not using your children’s capital gains exemption and simply paying the government. I’d rather pay my children.

Warning. This strategy involves passing land down to your children. Once it’s in their hands, nothing is forcing them to give it back to you. Not to mention if your children get divorced during these three years’ it could cause some headaches. You’ll also need to trust your children to follow through with the plan and give you back the proceeds of the land sale.

Figuring out how much your non-farming children should receive when you pass away compared to your farming child is tough. As I’m sure you’ve heard, fair doesn’t always mean equal when it comes to farm transition planning. To help you get started on coming up with a “what is a fair amount,” here’s a formula you can use. Keep in mind; this is only a starting point, your farm and situation may require this formula to be tweaked, especially with land prices continuing to rise.

[(A) – (X) – (Y) – (Z)] / Number of children you have

(A) Your total net worth (farm and non-farm assets)

(X) Your total tax bill if you’d convert all your assets to cash (imagine selling your farmland, equipment, inventory, RRSP, home, etc. how much tax would you pay?)

(Y) Your total debt (farm and non-farm debt)

(Z) The sweat equity your farming child has built up over the years but hasn’t been compensated for it

Here’s an example:

($6,000,000)-($1,000,000)-($500,000)-($200,000) = $4,300,000

$4,300,000/3 = $1,433,333

Here’s your theoretical starting point, $1,433,333*. Your farm child gets the $5,000,000 farm, and the other two non-farming children receive $1,433,333 each for a total of $2,866,666. You have $1,000,000 of non-farm assets, so you’re short by $1,866,666 to “make it fair.” How could you fund the shortfall?

a) Give farm assets to your non-farming children

b) Have your farming child make payments to their siblings after you’ve passed away to cover the shortfall

c) Have the farm borrow money to fund the shortfall

d) Start withdrawing additional funds from the farm and setting them aside for the non farming children today

e) Purchase life insurance

f) Etc.

*Make sure you tweak the formula if you’ve already gifted some assets to your non-farming children. For example, if you paid for their university or gave them a down payment on their first home, those gifts should be subtracted from their “What is fair” total.

AMT is short for Alternative Minimum Tax (it’s a hidden tax you may have to pay in the year you sell your farm). AMT is very complicated, here’s the simplest explanation – it’s a tax you pay if your total personal income is high, but due to exemptions and credits, your taxable income is low.

Here’s an example. You sold some land for $1,100,000 to your neighbour. You had purchased this farmland 40 years ago for $100,000. You have a total income of $500,000 (only 50% of capital gains are added as income). However, due to using your $1,000,000 capital gains exemption, your taxable income is now $0.

It may seem like this transaction won’t cost you any taxes, but wait a minute. AMT gets calculated in the background, and since there’s such a discrepancy between your total income and your taxable income AMT comes into play.

So now what? Well, in a case like this, you may need to pay up to $50,000 in AMT (alternative minimum taxes) but it’s not all bad news. AMT can be considered a prepayment of your taxes. Over the next seven years, if you owe taxes, you won’t need to pay them if you still have an AMT balance remaining.

Here’s an example. You paid $50,000 of AMT in 2021. In 2022 you owe $10,000 of taxes. You won’t need to pay these because you still have an AMT balance. It will drop to $40,000. The next year in 2023, you owe $15,000 of taxes; again you don’t pay them because of your AMT balance. It drops to $25,000. You can do this for seven years or until your AMT balance is zero.

WARNING: If you don’t use your full AMT balance before the end of the 7th year or you pass away, you won’t be able to recover those prepaid taxes. That is why it’s essential to make sure you have a future tax strategy before selling any farm assets.

If it’s a foregone conclusion that you’ll be selling your farm and you’re in between the ages of 60 & 64, I’d recommend you do so sooner rather than later for the simple reason that you’ll miss out on one year’s worth of OAS if you wait until 65.

You may say it’s not worth rushing things to make sure you receive your OAS. I agree, but if you’re procrastinating, get moving!

To qualify for your full OAS, your net income must be below $81,761 (for 2022). For every dollar you earn above $81,761, you must pay 15 cents of your OAS back to the government. This means if your income reaches $133,141, you’ll have lost all your OAS.

Even if you have enough capital gains exemption room to avoid paying any taxes on the sale of your farm, if you are receiving OAS, it will still get clawed back.

You might be wondering. I have my capital gains exemption; my income won’t be that high because I’ll be able to shelter my gain. That is true, but to qualify for OAS they look at your net income (not your taxable income). Your net income will be very high as it will reflect the sale of your farm, whereas your taxable income will be low as it will take into consideration your capital gains exemption.

So, there you have it. OAS may only be about $8,002 per year ($16,004 if you take into consideration your spouse). It may not be much, but if you can add an extra $16,004 to your income by selling a year earlier, why not? CRA has taken plenty from you over time, don’t let them take another sixteen thousand if you can avoid it.

What does retirement look like to you? Are you still working on the farm? Have you moved to town? Are you travelling the world? How much income will you need from the farm? If you’re selling to your child, how much of a discount can you give them, if any?

Before you start contemplating the transfer of your farm, it’s essential to reflect on your own retirement and make some projections. It’s the first thing you need to tackle because there’s no sense talking about transferring the farm if you need every single penny of income it generates for your own retirement.

Since farming has so many unique tax rules, don’t make these projections on a napkin. You should work with a Certified Financial Planner (CFP®) and preferably one that specializes in the ag industry. For a list of qualified farm advisors, visit https://www.cafanet.ca/.

To figure out how much you’re spending today and how much you’ll need in retirement, we have a cash flow analysis Excel sheet available on our website for you to download.

Gifts from parents are not part of marital property. For example, if you gift your child cash and they leave it in a separate account (not a joint account with their spouse), it will most likely be protected in the event of divorce.

It’s the same situation with your farm. If you gift your farm to your children, it won’t be part of their marital property.

The downside of gifting is you can’t bump up the cost base of your farm so your child may have to pay additional taxes in the future if they sell it. It’s a little complicated but I’ll try to keep it simple by going over two scenarios

Scenario 1:

You sell* (don’t gift) the farm to your child. You’re able to increase the cost base of the land by using your capital gains exemption but the farm is now part of marital property.

Example: you purchased the farm for $250,000, today it’s worth $1,250,000. You “sell” it to your child for $1,250,000 bumping the cost by $1,000,000 to $1,250,000 by using your $1,000,000 capital gains exemption. If your child sells the farm in the future, their capital gain will be the increase in value from $1,250,000 and on.

*You need to “sell” the farm to use your capital gains exemption, but your child doesn’t need to pay you anything, more on this below.

Scenario 2:

You gift the farm to your child. Since it wasn’t a sale, you’re not able to use your capital gains exemption to increase its cost base.

Example: you gift the farm valued at $1,250,000 with a cost base of $250,000 to your child. If your child sells the farm in the future, their capital gain will be calculated starting at $250,000 vs. $1,250,000. This results in additional taxes paid when compared with scenario one.

The question becomes what’s important to you? Tax-efficiency or protecting assets from marital breakdowns?

How can I “sell” the farm to my child but not receive any cash? In lieu of cash, you’re able to receive a promissory note from you child. This adds an extra layer of protection, because the promissory notes states your child owes you $$$ which you can request at anytime. This is helpful in the event your child goes through a divorce because you could call the note. Calling it would reduce the value of your child’s family net worth because they would owe you for the land you sold to them. This would reduce what is being split due to divorce. Once everything is finalized you could sell the land back to your child.

Assuming all goes well and your child doesn’t get divorced you’re able to forgive the promissory note at death so you’ve essentially gifted the land to your child with the tax benefits of having sold it and used your capital gains exemption to bump up its cost base.

Thinking of a world without taxes helps you narrow your focus to what’s important to you. Often, without even realizing it, I’ve seen farmers talk themselves out of what’s important to them over the fear of the attached tax consequences. They will instead suggest a different direction which they feel is more tax-efficient even though it’s not really what they’d ultimately like to see.

My suggestion – Tell your team of professionals exactly what you’d like to see with your farm. This gives us a starting point. We can then come back and tell you “your plan will cost you $$$ in taxes, however if we change this one variable your tax bill will be reduced by $$$.” It is at this point where tax consideration should come into play. Are you willing to pay this tax bill to accomplish your goals or would you like to tweak your vision so your overall tax bill gets reduced?

As an advisor coming up with ideas, I’m at least starting from a position that I know you’re interested in vs. randomly throwing ideas at you that are tax-efficient but may not be accomplishing any of your goals.

Transition plans will often include life insurance because it’s one of the simplest ways to provide your non-farming children with additional assets at death.

If you’re purchasing or already own life insurance, make sure your farm corporation owns it. The benefits of having your corporation own the life insurance and make the payments are:

For example, if the cost of insurance is $5,000/year and you’re paying for it personally, your corporation would have to write you a cheque of $6,000+ to net you $5,000 after personal taxes. Having the corporation make the payments directly saves you personal tax.

2. When you pass away the death benefit can exit your corporation tax-free via the capital dividend account

I should clarify, most likely your full death benefit will be able to exit the corporation tax-free. The tax rules are beyond the scope of this guide, but here’s a simple rule of thumb. If you purchase permanent life insurance and pass away within the first 10-20 years, the corporation may only be able to withdraw 80% of the death benefit tax-free. If you live well into your 90’s the corporation will most likely be able to withdraw the full death benefit tax-free via the capital dividend account. It’s important to review this with a financial planner who specializes in farmers before purchasing life insurance inside your corporation.

Common myth: You can write off the insurance payments. That’s incorrect. You’re only allowed to write off the payments if you have a letter from a lender saying they required you to purchase life insurance on your loan.

The best way to start a family conflict is to die without telling all your children what your intentions were. Even if you made your farming child aware of your plans, that might not be good enough. Having not been in the loop, your non-farming children might feel alienated and think their farming sibling(s) have influenced you in some capacity.

If you don’t have any farming children taking over the farm this isn’t as crucial (however I still recommend you share your plans with your children regardless), but if you have one child taking over the farm it imperative that you have a family discussion with all your children before passing away.

Assuming you want to maintain family harmony after your passing, having a family discussion gives you a chance to explain why you’re doing things a certain way. Even if some of your children disagree with your reasoning, they will at least have heard it from you as opposed to your will. It will also allow them to voice their opinion which you can address while living. You can’t do much explaining once you’ve passed away.

Talking about your plans today is your best shot at maintaining family harmony after your passing

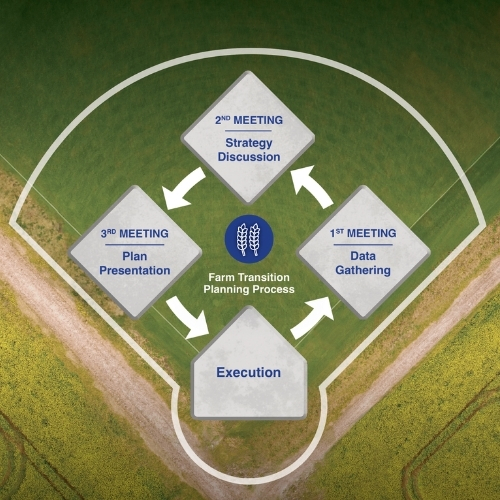

The hardest part of putting together a transition plan is getting it started. You may have attended a few seminars in the past, you may have talked with a few neighbours, you’ve downloaded this guide, but none of that actually gets you started.

I don’t blame you; it can seem very intimidating to get going because there’s so much info out there.

My most important tip is also the simplest one – start by grabbing a coffee with an advisor. Most Advisors don’t charge for an introduction meeting, and it gets the process rolling.

I always outline a plan when discussing transition planning because knowing the steps helps you to continue moving forward because you know what’s next. I’ve seen too many farm families start the transition planning discussion only to get stuck after about a month.

With no guidance, with no quarterback leading the process, it’s hard to stay on track.

I tell farmers, plan to be working at this for at least 18 months, that’s usually how long it takes from start to finish to finalize a transition plan. Afterward, plan to review every three years because things are continually changing.

If you’re ready to start, if you’re looking for peace of mind knowing you’ve done the best possible planning for your farm, don’t hesitate, let’s grab a coffee.

The information contained herein was obtained from sources believed to be reliable. However, we cannot represent that it is accurate or complete. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell any securities. The views expressed are those of Colin Sabourin, Certified Financial Planner, and Investment Advisor, and not necessarily those of Harbourfront Wealth Management Inc., a member of the Canadian Investor Protection Fund.