Retirement Specialist, Portfolio Manager, Certified Financial Planner

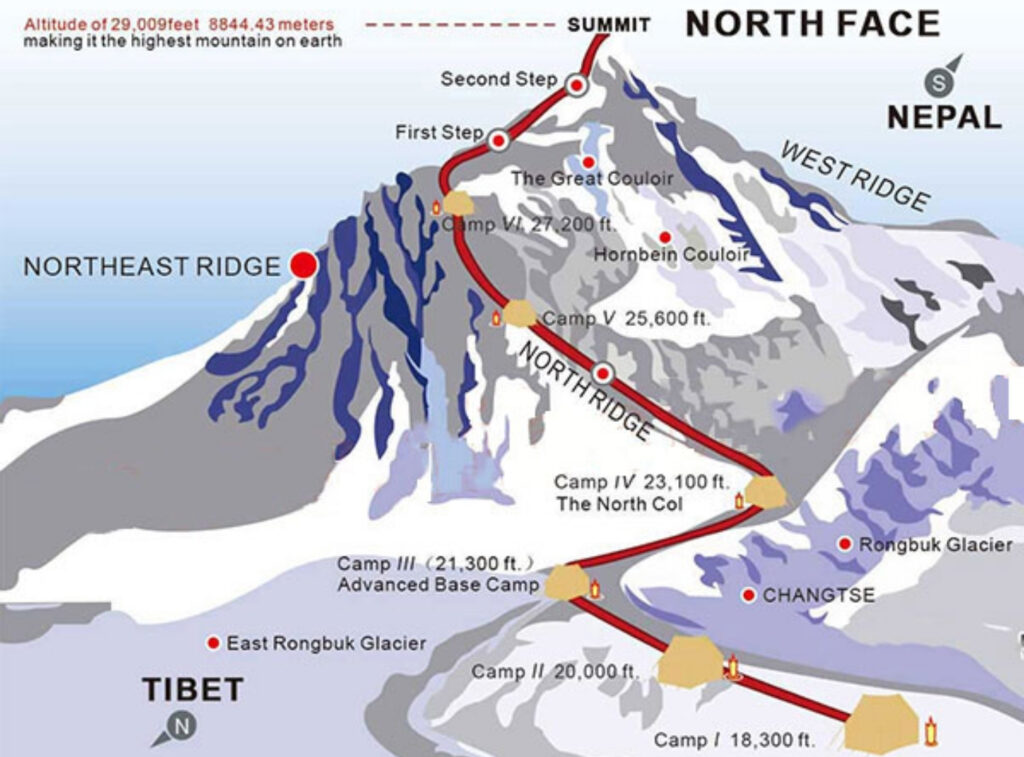

Let’s imagine for a moment that you were a mountain climber trying to summit Everest. It’s a pretty big mountain, so there are camps set up along the way to rest.

The end goal of summiting is quite apparent, but what’s just as important as making your way up is knowing exactly where you are on the mountain. If you think you’re at Camp 4, but you’re still only at Camp 1, that’s a big difference in terms of how many supplies you’ll need to bring along with you. You still have a long way to go if you’re still at Camp 1, so that means you should pack some extra food!

When it comes to planning for one’s retirement, I’ve come to realize that a lot of people have no idea where they are in terms of reaching their goal.

Where are you at today? Camp 1, Camp 2, 3,4… If you don’t know where you are in terms of reaching your retirement goals, how can you make a plan to get to where you want to be? That’s like the mountain climber trying to reach the summit without having any idea if he is still at base camp or halfway up the mountain. That will be a difficult climb!

So how can you figure out if you’re on track to achieve your retirement goals? The first step would be to put together a snapshot of where you stand today.

Your brother is finally getting married, and his wedding starts in an hour. It’s a 100km away, so if you leave immediately, you’ll be able to drive 100km/h and make it on time. That’s cutting it pretty close, but doable.

On the other hand, if you leave a half an hour late, you’d have to drive 200 km/h to arrive on time. Your odds of getting into an accident or receiving a speeding ticket would go up significantly. You’re probably better off showing up late and alive rather than risking the drive at those speeds.

It’s the same idea when it comes to saving for your retirement. A lot of people hate having debt, and I’ve often heard statements such as “I’ll start saving once my mortgage is paid off.” They then pay off their mortgage at 55 and are astonished by the amount that they’ll need to save by the time they are 60 to retire.

Let’s say you expect to live until you’re 90. Do you think you can save enough money between the ages of 55-60 to last you from 60-90? There’s something about that math which won’t add up and it’s far more likely that you’ll be working longer than you wanted.

We’ve all heard that compound interest can be your best friend, and a contribution towards your savings today, even if comparatively small to what you could put away in the future, will have a significant impact on your retirement nest egg. Every day that savings are delayed increases the burden on one’s future self to make up the shortfall. When it comes to planning for my retirement, I’d rather have my foot lightly on the gas over my working career rather than the pedal going through the floor, trying to catch up on missed retirement contributions.

The big question you need to ask yourself is, “How was the debt accumulated?” If you have a balance owing on a line of credit or a credit card, is it because you were living above your means? If so, retiring with that debt can be problematic.

Once you retire, you will likely be on a fixed income and credit card debt can put you in a tough financial position. If you’re receiving a monthly pension, it’s not like you can work some overtime and use the funds to pay off your debt.

If you’re planning on generating your income from an investment portfolio, you can’t use it as a piggy bank to pay off your debt whenever you live above your means. There are tax consequences on withdrawals and you need the funds to last throughout your retirement. Focus on paying off the debt before you retire and keep these types of debts under control in retirement.

On the other hand, if you have a mortgage against your home or a balance remaining on a car loan, it may be feasible to carry these debts in retirement. These types of debts generally have set payments and are a lot easier to factor in your budget.

Tip: Start by paying off any high-interest debt such as credit cards, vehicle loans, and unsecured lines of credit.

Once you’re retired, your income will likely comprise your pension, RRSP/RRIF, CPP, and OAS. The problem with all of the sources of income is that they’re taxable.

If you want to withdraw funds from your portfolio to go on a trip, buy a new vehicle, or complete a renovation, it will need to come from your RRSP or RRIF. Withdrawing from these accounts will increase the amount of tax you have to pay and may cause you to jump into a higher tax bracket.

By building up your TFSA today, it will provide you with a source of tax-free income in retirement. Rather than having to borrow to buy a car or pay tax on an RRSP withdrawal, you can withdraw the funds from your TFSA instead without any tax consequences.

Many people believe a TFSA is simply a savings account that you get at the bank where your interest grows tax-free. Although technically correct, a TFSA can be a much more powerful tool that gives you access to investment options such as stocks, bonds, ETFs, mutual funds, and GICs, just to name a few.

The RRSP has been getting a lot of negative attention over the last few years as people now realize that they have to pay tax on amounts withdrawn today and in retirement. Does that mean you should avoid the RRSP all together and focus your retirement savings in a TFSA instead?

In some cases, that absolutely makes sense, but if you’re in a high tax bracket today than RRSPs are still beneficial.

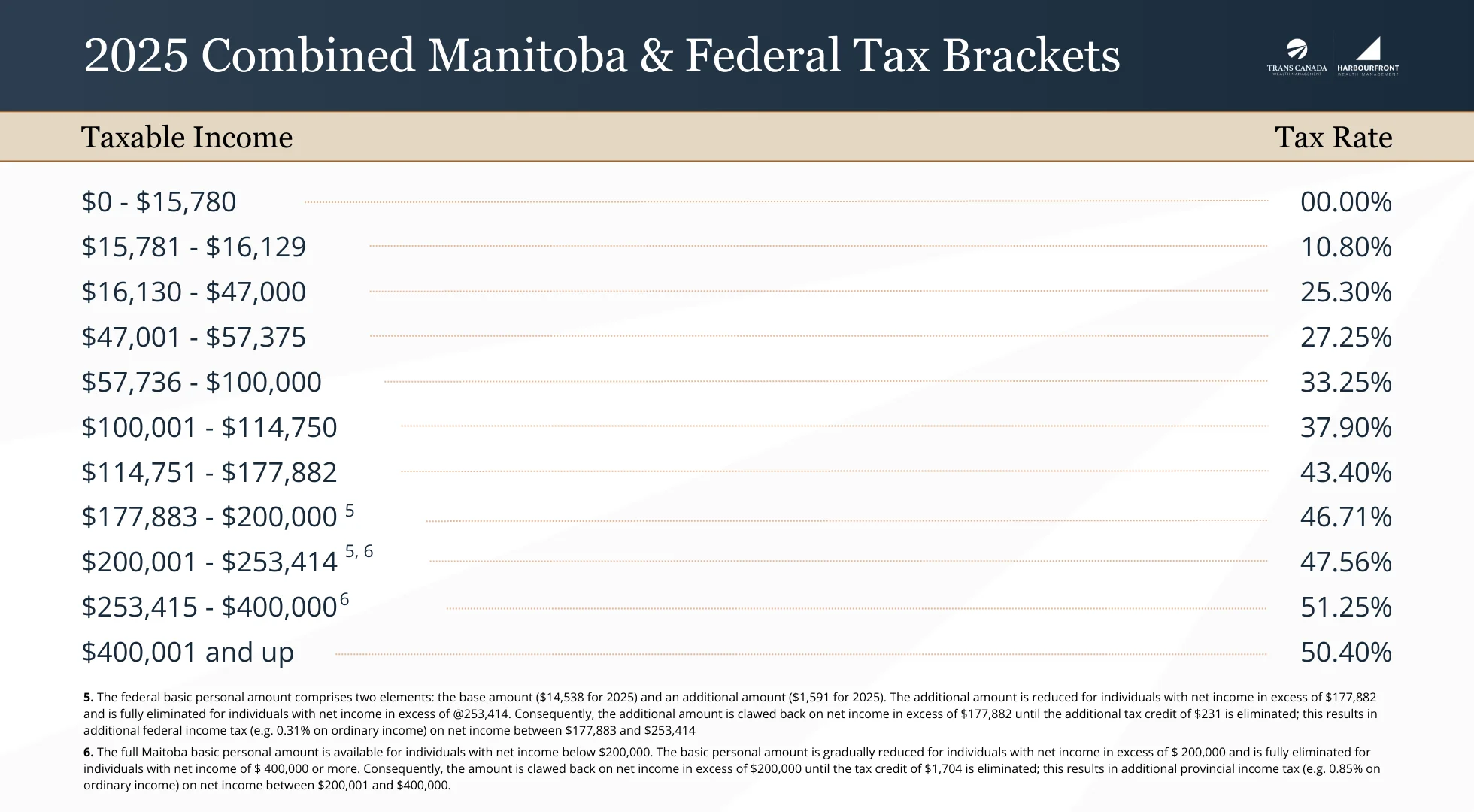

At its core, a contribution to an RRSP will reduce your taxable income by your corresponding marginal tax rate. For example, if you make $110,000 per year you will fall under the 37.9% marginal tax bracket as per the combined 2025 Manitoba and Federal tax rates.

If you make a $4,000 contribution to an RRSP, your taxable income will drop to $106,000. This would result in a tax refund of $1,516 ($4,000 x 37.9%).

The rates above reflect combined Manitoba and federal taxes. If you live in a different province, use the link below to view your province’s combined tax brackets.

Let’s assume that when you retire, you’ll have an income of $50,000 per year including your pension, CPP, and OAS payments. When you withdraw that same $4,000 from your RRSP, it gets added to your income. This would increase your income from $50,000 to $54,000, and you would fall under the 27.25% tax bracket. This $4,000 withdrawal from your RRSP would cost you $1,090 in taxes ($4,000 x 27.25%).

In this case, you would have tax savings of $1,516 when the $4,000 was deposited into your RRSP, and you would pay $1,090 when that same $4,000 was withdrawn from the RRSP. That’s a difference of over $400 in your pocket!

**Assuming Federal and Manitoba combined tax rates**

The majority of people who are saving for retirement will have an RRSP and a TFSA. Within those accounts, there will be a combination of stocks, bonds, GICs and other investments.

Without having to change your risk tolerance, you can have your accounts grow a lot more if you’re tax-efficient. To find out how to properly structure your accounts to be as tax efficient as possible.

How much will your retirement lifestyle cost? Will it be sustainable throughout your retirement? Most estimates predict a spending rate of 70% of your pre retirement income, although I would recommend you personalize your plan.

Meet Bob and Julie

Imagine Bob and Julie each made $100,000 per year. By rule of thumb, each of them can expect to spend $70,000 per year once they are retired.

Bob’s idea of retirement includes:

Julie’s idea of retirement includes:

These retirements look entirely different. Bob might be able to live off $50,000 per year which would allow him to retire many years sooner. On the other hand, Julie’s retirement will likely cost her more than $70,000 per year, so she’ll run out of money if she doesn’t put more away or work longer.

You’ve been plugging away at your job for the last 20 years and you’re ready to enter the next chapter of your life. You’ve decided that you’d like to retire on the earliest date on which your pension isn’t reduced. In this case, that date is November 1 and you expect your year-to-date income to be $100k. You’ve also decided that you’d like to withdraw the lump sum from your pension to be certain that you will have something for your estate if both you and your spouse pass away. You will be retiring with a full 50 days of vacation as well as banked sick time.

The Issue

Upon retiring you will be paid out your sick time, vacation days, a potential severance, as well as the taxable portion of your lump sum pension. If you don’t have any RRSP room remaining, you will have no means to shelter this additional income.

Let’s assume that your sick time, vacation, and severance account for an additional $50k in income. Let’s also assume that the taxable portion of your lump sum pension is $200k. You’ve just added a quarter of a million dollars of income on top of the $100k you already earned in salary for the year.

The Strategy

Instead of retiring on November 1, you might want to consider pushing your retirement to December 15. It should still give you time to get all your Christmas shopping done ;). Let’s assume your year-to-date income is $115k by that point. It usually takes a couple of weeks to receive payment on your vacation, sick days, and severance, which is still $50k. The pension takes a little longer to transfer over so that income will be taxed in the following year. Your income in the year you retire would be $165k ($115k salary + $50k in payments). Your income in the following year would be the $200k taxable portion of your pension.

The Payoff

As per current Manitoba and Federal tax rates, you can expect to pay $143,070 in taxes based on an income of $350k. However, if you split this income as per the strategy outlined above, your tax bill would be significantly reduced. You would be taxed $52,246 on an income of $165k in the year you retire as well as an additional $68,168 on your $200k income the following year. You’ve just saved over $22k in taxes by moving your retirement date out by 45 days. What’s even more stunning is you saved this money all the while earning an additional $15k over two years.

When should you start drawing down your RRSPs?

Upon your death, your RRSP or RRIF is transferable to your spouse tax-free. Upon the second spouse’s death, the entire amount of the RRSP and RRIF becomes taxable. That can leave the estate with a huge tax bill.

In some cases, it may be beneficial to begin drawing on your RRSP or RRIF sooner rather than later, even if you don’t need the money. By withdrawing more today, you may be able to pay less tax overall.

It’s without a doubt one of the most discussed topics around the watercooler. Should you take your CPP as soon as you are eligible at 60, or are you better off waiting until you’re 65 or even 70.

There is no right or wrong answer as it’s a matter of personal preference, but there are some instances where it absolutely makes sense to take it or early or wait.

Some of the reasons you should take your CPP early include:

Some of the reasons you should wait to take your CPP include:

The correct time to begin your payments is different for everyone, but there are definitely some things to be aware of before making your decision.

Companies will often offer employees early retirement packages to encourage them to retire. This is usually done when the company is looking to cut costs and reduce staff.

Before making a decision, there are many questions to be addressed. All of which are specific to individual preferences and circumstances. Here are eight such considerations to factor in before making your final decision.

One of the common concerns we come across with new retirees is how to structure their investment portfolio.

Some want to become extremely conservative with their investments as they don’t want to risk losing any money. The problem with this approach is that once you factor in inflation, you actually end up losing money in a lot of cases.

Others want to maintain the same aggressiveness they had while they were saving for retirement. This approach can see you heading back to work if there is a huge downturn in the market, as we saw during the financial crisis in 2008 and the COVID-19 Pandemic in 2020. So how do you get around both of these issues? By using the Bucketing Strategy.

For those of you lucky enough to have a defined benefit pension plan, you may have to decide whether to take your pension as a monthly income or as a lump sum payout upon retiring. There isn’t a universally accepted answer when deciding between these two options, as it mostly depends on your personal circumstances. Just because a retired coworker went with one option, doesn’t mean the same choice is right for you.

Remember, once you choose, your choice cannot be reversed. If you decide to take the monthly income, you can’t ask your pension for an extra lump sum payment the next time you want to go on a vacation. In much the same way, you can’t pay back the lump sum to your pension if you feel that managing it yourself is too much work.

How do you decide?

Several factors could affect your choice. An excellent place to start would be to build a financial plan with a side-by-side comparison of both options. This should include your overall expected retirement income from both your pension and savings. Once you know what you have to work with, I highly suggest reviewing the pros and cons of each option before making a decision.

If you choose the lump sum payout option from your pension, it’s not as simple as receiving a large cheque. There are many factors to consider, which could affect the taxation and the eventual payout from your pension.

If you don’t have any pension income, be sure to convert a portion of your RRSPs into a RRIF once you turn 65. After the age of 65, RRIF withdrawals are considered pension income which qualifies you to receive the pension credit.

If you withdraw $2,000 per year from your RRIF after the age of 65, you will receive a pension credit of $398 on your taxes. These RRIF withdrawals are also eligible to be split with your spouse. If your spouse doesn’t have any pension income, I would suggest you withdraw $4,000 per year from your RRIF instead. This income would be split evenly with your spouse and you’d both be eligible to receive the $398 pension credit.

Every investor knows that it makes sense to buy low and sell high. Although when push comes to shove, it’s very difficult to put into practice.

When the stock market is down, every news channel you turn on will be telling you the world is ending. This has happened time and time again, such as during the financial crisis in 2008 and the COVID-19 pandemic in 2020.

Looking back, these were great opportunities to take advantage of lower prices in the stock market. Although at the moment, it constantly felt like things were going to get worse, the markets inevitably recovered.

As long as you have a long investment time frame (5+ years), these are great opportunities to buy into the market at bargain prices. The market will crash again in the future, be ready to take advantage of it.

Once retired, people tend to become more conservative with their investments. After all, it is their nest egg and they would like to protect it.

Having said that, it’s important that your portfolio still has an element of growth to it due to the effects of inflation. Inflation can be summarized as the increase in the cost to purchase the same items on a year-over-year basis. The price for a jug of milk today is substantially higher than it was 25 years ago.

Canada’s historical inflation rate has hovered around 3% and as of this writing sits at 2.8%. That is to say; if you have $100,000 today, you will need $102,800 next year to purchase the same amount of goods. If this $100,000 is left in a savings account or a GIC earning less than 2.8%, you will have lost purchasing power on a year-over-year basis.

Your portfolio must grow at least at the rate of inflation to ensure you don’t lose any purchasing power.

Do you recall the last time you turned off the nightly news and told yourself, “I feel great about where the world is headed!”? It’s probably been a long time. You’ll be hard-pressed to come away with one feel-good story because the fact of the matter is those stories don’t sell.

All this negativity can impact your portfolio because it weighs heavily on your emotions. To combat this, I started a list back in 2012 of all the negative, portfolio-destroying, headlines every year.

2014: Oil Crash

2015: China’s growth stalling

2016: Brexit & Trump’s election victory

2017: North Korea’s Missile Tests

2018: NAFTA & China Trade War

2019: Trump Impeachment

2020: COVID-19

2021: Lockdowns

2022: Inflation

2023: Silicon Valley Bank Collapse

2024: US Election Year Volatility

2025: Tariffs

Each one of these headlines would make you want you to cash in your portfolio and stuff the money under your mattress. Heck, I feel the same way when I turn on the news and there is a new red flashing headline talking about how the world is going to hell in a handbasket.

Avoid investing by “feel”

The most important part of investing is taking emotions out of the equation. Markets will rise and fall regardless of how we feel about them on any given day. If you had stuffed your money under the mattress back in 2020 during the COVID-19 market declines, you wouldn’t have just missed out on years of growth, but you would undoubtably have major back pain by now as well. With a long-term investment strategy in place, there is no need to panic over every headline or market swing. Turn off the TV, avoid the noise, and save yourself the stress.

Remember: your portfolio is like a bar of soap, the more you handle it, the smaller it gets. In other words – stick to your plan, stay patient, and enjoy life!

When it comes to scoring well in golf, it’s about how many bad shots you can avoid, rather than how many good shots you can hit.

If you can stay out of trouble and play the “smart” shot, you’ll likely score a lot better. It’s the same when it comes to investing.

If you have a retirement plan that says you need to average 4% per year to achieve your retirement goals, there’s no sense in taking huge risks with your portfolio to earn that 4%.

If you hear of a hot junior mining stock tip from a co-worker, is it really worth moving out of your portfolio to try to make it big on this stock?

If it works out, then great.

But, if it ends up being a clunker, you’ve just scored a double bogey with your portfolio.

Now you’re behind on your retirement goals, and you’re in catch-up mode, which means “going for it” a lot more. This can produce more misses, which could put you even further off track.

There are tools available to help construct your own retirement and investment plan, but I would strongly recommend using the expertise of a Certified Financial Planner.

As exciting as retirement can be, it can also be nerve-racking if you haven’t accounted for all factors involved. Nobody wants to be in a position where they have to return to work in 10 years because they failed to take into consideration all aspects of their retirement.

A Certified Financial Planner can provide you with the peace of mind that your plan has been well thought out and is sustainable throughout your retirement. Additionally, they can make sure that all aspects of your plan (taxes, investments, cash flow…) are working together to keep more money in your pocket.

Thank you again for reading over our 20 Retirement Tips. We hope the tips were helpful and gave you insight into creating the retirement you deserve.

These 20 Tips are designed to inform you of everything that goes into a thorough retirement plan. By putting these tips into action, you could drastically change the lookout of your retirement.

If you have any concerns about your retirement and want to ensure a financially secure future, don’t hesitate to give us a call today!

Our team of retirement experts is dedicated to helping you get answers to any questions you may have. Let us guide you through the process and help you make informed decisions about your financial future.

There is never a cost associated with initial phone calls or meetings.

We would be more than happy to help!

Trans Canada Wealth Management is a Winnipeg-based Financial Advisory Team with Harbourfront Wealth Management. The team works with pre-retirees and retirees seeking guidance on retirement, investments, and taxes.

The views expressed are those of the advisor(s) featured and not necessarily those of Harbourfront Wealth Management Inc., a member of the Canadian Investor Protection Fund.